Chinese yuan and U.S. dollar banknotes are seen in this illustration taken on Feb. 10, 2020. (Dado Ruvic/Illustration/Reuters)

News Analysis

A longstanding plan by China and Russia to replace the U.S. dollar as the world’s reserve currency has had a string of recent headline-grabbing successes, as China methodically builds a rival monetary system that has been dubbed “Bretton Woods III.”

This currency initiative is the financial component of the Beijing regime’s strategy to gain influence over global energy supplies and overcome its key weakness as an energy-poor country—a strategy that appears to be working.

“Given the increased weaponization of the dollar for national security purposes, and the growing geopolitical rivalry between the West and revisionist powers such as China, Russia, Iran, and North Korea, some argue that de-dollarization will accelerate,” economist Nouriel Roubini wrote in a Financial Times op-ed, titled “A Bipolar Currency Regime Will Replace the Dollar’s Exorbitant Privilege.”

According to the International Monetary Fund (IMF), Bretton Woods III is “a new monetary order centered around commodity-based currencies.” This system features a network of agreements among China and commodity-exporting countries to trade in Chinese yuan or other currencies besides the U.S. dollar.

But dethroning the dollar as the world’s reserve currency is a side benefit to China’s goal of establishing reliable long-term access to the energy supplies it so desperately needs. Countries that have thus far agreed to accept Chinese yuan as payment for oil include Russia, Iran, and Venezuela. Together, these three oil exporters represent 40 percent of the world’s known reserves; all are currently under embargo by the United States.

Meanwhile, China and Brazil have struck a deal to ditch the U.S. dollar in trade transactions in favor of their respective currencies.

What Roubini called the “weaponization of the dollar” refers to the United States’ habit of using its financial authority to punish its adversaries, most recently ousting Russian banks from the foreign exchange-settlement system known as the Society for Worldwide Interbank Financial Telecommunication (SWIFT). Some analysts, however, warn that America’s politicization of the global dollar system is compelling an ever-larger number of nations to seek alternatives, and China appears happy to oblige them.

Most recently, and perhaps worryingly for the United States, Saudi Arabia, the world’s largest oil exporter, has stated its willingness to consider using yuan for oil exports as well. China scored a strategic coup on March 10 when it brokered a diplomatic détente between Saudi Arabia and Iran—with no United States involvement.

Much of the reason for the dollar’s global dominance is the result of “petrodollars,” the outcome of a protocol that has, since the 1970s, dominated trade by Saudi Arabia and other oil-producing countries in dollars. While oil, gas, and other forms of energy make up the majority of the world’s commodity markets, most other commodities, including minerals and agricultural goods, are also priced and traded in dollars.

That’s forced countries around the world to hold dollars in order to trade in these markets, and this demand for U.S. dollars and Treasury securities has reduced the cost of borrowing for the United States even as government spending and deficits reach new heights.

Why China’s Plan Might Fail

Many financial analysts insist that the dollar’s dominant position is unassailable for many years to come. While America’s economic dominance has declined from half of the world’s gross domestic product (GDP) in 1945 to about one-quarter today, and while China has succeeded in establishing yuan-denominated trading deals with key commodity exporters, the dollar’s role in global finance is still paramount.

“There’s such a huge head start for the dollar on any dimension,” including foreign exchange, trade invoices, and debt and equity markets,” economist David Beckworth, a research fellow at George Mason University, told The Epoch Times. “Any proposal for an alternative currency that would compete with the dollar would have to scale up in such a size that it doesn’t seem feasible.”

The dollar’s share of global debt markets isn’t only dominant but increasing.

In order for China to become a reserve currency, “it would have to completely open its capital markets so that money can flow across the border into and out of China without any kind of restrictions … and that’s something that the authoritarian regime that’s in power does not want to do,” Beckworth said.

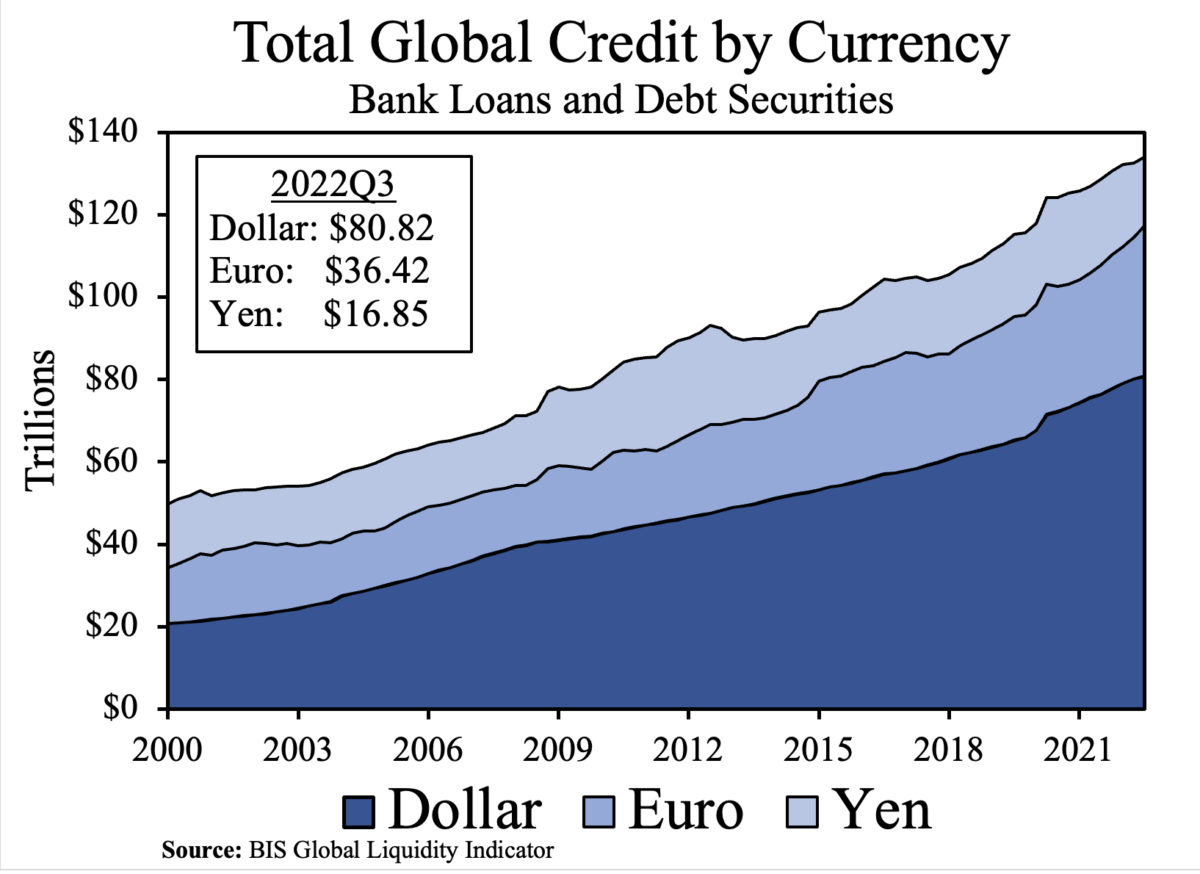

Currently, about half of the world’s trade and about 60 percent of all central bank foreign-exchange reserves are denominated in U.S. dollars. The euro, the dollar’s closest competitor, is a distant second, at 20 percent of central bank reserves. The share of reserves held in yuan is 3 percent.

In some areas, the dollar’s role is steadily declining. Its share of global reserves has fallen to 59 percent in 2022 from more than 70 percent in 2000. Still, to replace the dollar, some analysts say a currency must have attributes that only the United States possesses.

A key question, then, for those who would accept Chinese yuan in trade is: What do they do with them? The attractiveness of dollars isn’t only that they are widely accepted but also the prevalence of investment opportunities.

The United States is among the most open economies in the world, and investment options for dollars range from demand deposits to bonds, stocks, and real estate. China, by contrast, is a relatively closed economy with currency controls and limited investment options. U.S. equity markets comprise about one-third of all global stocks; China’s stock market comprises less than 8 percent.

In addition, dollars are featured in about 90 percent of all foreign-exchange transactions. Even after getting a boost from the Russia/dollar embargo, yuan were featured in only 7 percent of foreign currency trades, behind the euro, the British pound, and the Japanese yen.

Another key shortcoming for the yuan is that it lacks a history of stability. Even with America’s more recent history of profligate spending and interest-rate manipulation, the dollar has built a reputation over centuries as a credible and dependable currency. Within China, there is a constant risk of “capital flight,” as the wealthy attempt—amid currency controls on the yuan—to move their savings abroad to safer havens such as the United States.

In addition, China would have to run persistent trade deficits in order to supply enough yuan abroad for global transactions, which is the opposite of China’s current export-led growth strategy, Beckworth said.

China’s trade deals are bilateral, while the dollar is in common use among all countries of the world, whether or not the United States is part of the transaction, according to noted economist Milton Ezrati, who is an Epoch Times contributor.

“The yuan is a long way from an international reserve currency such as the dollar,” Ezrati stated during an interview with NTD, the sister media outlet of The Epoch Times. “It might hurt Washington that China has supplanted the dollar in a relationship with Brazil or Saudi Arabia, or many countries that have joined the Belt and Road” initiative, a global infrastructure development plan launched by China across the developing world in 2013.

“I’m sure it does irritate them. Washington loves power,” he said, “and this is a slight erosion in that power. But I don’t think it’s a challenge to the dollar as the world’s reserve currency.”

Why China’s Plan Could Work

Roubini argues that China may yet succeed.

“Complete exchange-rate flexibility and international capital mobility are not necessary in order for a country to achieve reserve currency status,” he stated. “After all, in the era of the gold-exchange standard, the dollar was dominant in spite of fixed exchange rates and widespread capital controls.”

“While China may have capital controls, the U.S. has its own version that may reduce the appeal of dollar assets. … These include financial sanctions against its rivals, ” Roubini said. In some cases, such as during the Russia–Ukraine war, the United States has frozen or confiscated dollar assets held by foreigners.

While the dollar is simply backed by a promise of the U.S. government to pay, China’s yuan-based trade deals offer something of tangible value. On Dec. 9, Chinese leader Xi Jinping proclaimed to Saudi Arabia and other Gulf Cooperation Council (GCC) leaders gathered in Riyadh “a new paradigm of all-dimensional energy cooperation.”

“China will continue to import large quantities of crude oil on a long-term basis from GCC countries, and purchase more LNG,” he stated. “We will strengthen our cooperation in the upstream sector, engineering services, as well as storage, transportation, and refinery of oil and gas.

“The Shanghai Petroleum and Natural Gas Exchange platform will be fully utilized for RMB [renminbi] settlement in oil and gas trade.” (To distinguish, the renminbi is the official name of the currency; the yuan is a unit of the renminbi, but is the currency name used in international contexts.)

In short, China will provide technology, capital, and engineering services to build infrastructure, refining facilities, nuclear plants, oil extraction, etc., in return for a steady stream of oil supplies denominated in yuan.

In an effort to backstop the yuan, China has also been sharply increasing its purchases of gold. There also have been discussions about pooling several countries’ currencies into a basket currency that would be backed by commodities.

How China’s Success Could Hurt US

It would be “catastrophic” if the dollar lost its position as the global reserve currency, former U.S. Assistant Treasury Secretary Monica Crowley told Fox News.

“If Saudi Arabia decides to join with America’s enemies … and start trading oil in different currencies, that is going to undermine the entire global economic system.” The dollar’s loss of reserve status would “mean raging inflation, so much worse than anything we have ever experienced.”

In a report titled, “War and Commodity Encumbrance,” economist Zoltan Pozsar writes that “China is starting to dominate OPEC+,” or OPEC plus Russia and 10 other non-member nations.

“The U.S. has sanctioned half of OPEC with 40 percent of the world’s oil reserves and lost them to China,” he writes, “while China is courting the other half of OPEC with an offer that’s hard to refuse.” He warns that other countries could be boxed out of energy supplies that are increasingly being pledged to China.

The result, he argues, could be that China emerges as the central power broker for global energy. He cites as an example the decision by German chemical company BASF to shift its chemical operations from Germany to China, where it is able to access energy and raw materials at a much lower cost.

Added to this is the fact that China already dominates global mineral markets, having, for example, controlling stakes in the Democratic Republic of Congo’s cobalt mines, as well as a near monopoly on mineral refining. As the West attempts a shift from fossil fuels, which the United States has in abundance, to mineral-based energy such wind and solar, its dependence on China will only increase.